invested amount 2.61

equity share 1%

discount rate 1%

investors ROI 5 years

final payout $60

net present value $54

Internal rate of return 82%

1.0 Executive Summary

2.0 Situation Analysis

2.1 Market Summary

Target Markets

2.1.1 Market Demographics

Market Analysis

2.1.2 Market Needs

2.1.3 Market Trends

Market Forecast

2.1.4 Market Growth

Target Market Growth

2.2 SWOT Analysis

2.2.1 Strengths

2.2.2 Weaknesses

2.2.3 Opportunities

2.2.4 Threats

2.3 Competition

2.4 Services

2.5 Keys to Success

2.6 Critical Issues

2.7 Historical Results

2.8 Macroenvironment

3.0 Marketing Strategy

3.1 Mission

3.2 Marketing Objectives

3.3 Financial Objectives

3.4 Target Markets

3.5 Positioning

3.6 Strategy Pyramids

3.7 Marketing Mix

3.7.1 Services Offered

3.7.2 Price

3.7.3 Promotion

3.7.4 Service

3.8 Marketing Research

4.0 Financials

4.1 Break-even Analysis

Break-even Analysis

Break-even Analysis

4.2 Sales Forecast

Monthly Sales Forecast

Sales Forecast

4.2.1 Sales by Partner

4.2.2 Sales by Segment

4.2.3 Sales by Region

4.3 Expense Forecast

Monthly Expense Budget

Marketing Expense Budget

4.3.1 Expense by Partner

4.3.2 Expense by Segment

4.3.3 Expense by Region

4.4 Linking Expenses to Strategy and Tactics

Sales vs. Expenses Monthly

4.5 Contribution Margins

5.0 Controls

5.1 Implementation

Milestones

Milestones

5.2 Marketing Organization

5.3 Contingency Planning

1.0 Executive Summary [back to top]

GDK is a new products and services company specializing in creating

products for consumer and government entities. Its expertise is the developing and

researching inventions.

2.0 Situation Analysis [back to top]

GDK offers high-level expertise in international high-tech business development,

channel development, distribution strategies, and marketing of products. It focuses

on providing two kinds of international triangles:

Providing United States clients with development for European and Latin American markets.

Providing European clients with development for the United States and Latin American

markets.

This year we intend to take on consulting work in related markets, specifically the rest of Latin

America and the better markets in the Far East. We will also look for additional leverage by

taking brokerage positions and representation positions to create percentage holdings in

product results.

2.1 Market Summary [back to top]

GDK focuses on software, services. These are mostly larger companies, and occasionally medium-sized companies.

Our most important customers are executives in larger corporations. They are marketing

managers, general managers, sales managers, sometimes charged with international focus and

sometimes charged with market or even specific channel focus. They do not want to waste

their time or risk their money looking for bargain information or questionable expertise. As

they go into markets looking at new opportunities, they are very sensitive to risking their

company's name and reputation.

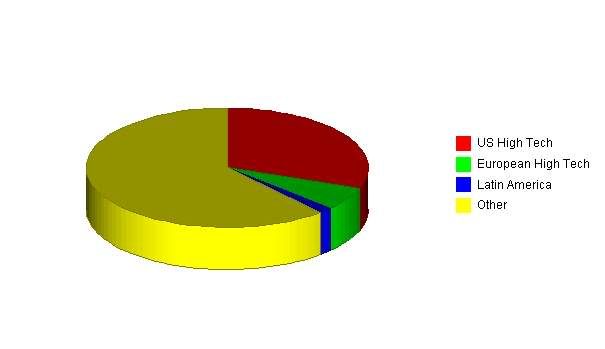

Target Markets

Click to Enlarge

2.1.1 Market Demographics [back to top]

Large manufacturer corporations: Our most important market segment is the large

manufacturer of products, such as Apple, Hewlett-Packard, IBM, Microsoft,

Siemens, or Olivetti. These companies will be calling on GDK for development functions that

are better spun off than managed in-house, for market research, and for market forums.

Medium-sized growth companies: Particularly in software, multimedia, and some related

high-growth fields, GDK will offer an attractive development alternative to the company that

is management constrained and unable to address opportunities in new markets and new

market segments.

Market Analysis

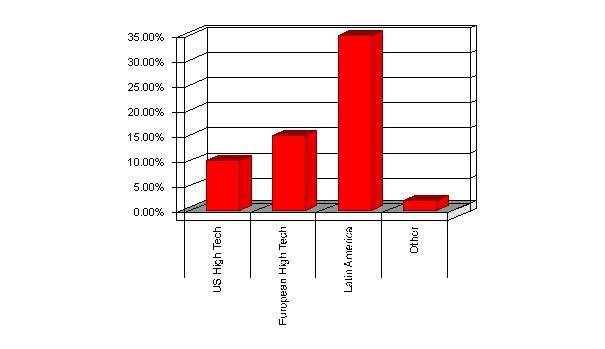

Potential Customers Growth 2004 2005 2006 2007 2008 CAGR

US High Tech 10% 5,000 5,500 6,050 6,655 7,321 10.00%

European High Tech 15% 1,000 1,150 1,323 1,521 1,749 15.00%

Latin America 35% 250 338 456 616 832 35.07%

Other 2% 10,000 10,200 10,404 10,612 10,824 2.00%

Total 6.27% 16,250 17,188 18,233 19,404 20,726 6.27%

2.1.2 Market Needs [back to top]

When a company, like those that are our clients, wants to open a new market, there is a

temporary need for very high-powered expertise. They need to establish distribution, evaluate

distributors' merits and problems, select and open new channels.

Our clients come to us for scalable, temporary expertise. They understand that our kind of

expertise would be very difficult and expensive to get from full-time, permanent employees.

Furthermore, their needs are temporary: the crunch is at the time of opening the new market

and setting up the channel; later on it is not as important.

From the point of view, as managers, our clients come to us at least in part because we reduce

their sense of risk in the management and politics of new market introductions. If things go

wrong, they have experts to blame. If things go right, they get the credit. There's the old

saying that "nobody ever got fired for choosing IBM," meaning choosing a highly respected

visible source for computers. We are that kind of low-risk option for opening new markets.

2.1.3 Market Trends [back to top]

We stand to benefit from some specific market trends:

There is a major trend towards internationalization. The Internet has brought a larger world

into direct communication with the manufacturers. Europe has created a major new unified

market, this time for real. Latin America is healthy and growing. Asia, despite recent setbacks,

is still a very good market. Our potential client base, the manufacturers, wants to expand into

new markets.

Communications technology is a new industry explosion. Also because of the Internet,

growth in communications technology items is explosive. Modems, network cards,

communications software, routers, cables, connectors, all of these are growing at 35% per year

and up. Margins aren't great in the more standard hardware categories, but growth is

enormous.

Contracting, consulting, and ad-hoc management teams are a trend. Even the larger

businesses are turning more frequently to temporary expertise instead of permanent fixed cost

employees. This is the latest new application of the buzzword "scalable." GDK is

an especially attractive alternative to our clients, because of the economic advantages of

variable vs. fixed costs, and the growing liabilities and overhead of taking on long-term

employees.

Market Forecast

Click to Enlarge

2.1.4 Market Growth [back to top]

The U.S. Association of Marketing Consultants reports a 30% growth in average revenues for

consultants focusing on marketing of products. We are a subset of this market,

possibly due for even higher growth than the mainstream. The local electronics industry

association in California reports a trend towards additional consulting solutions, as

manufacturers turn to variable cost solutions.

We talked to industry associations in Japan and several in Europe. Overall, the growth in

interest for moving into new markets is phenomenal. Tahahashi Sato, director of the local

association in Tokyo, told us "we don't have statistics, but the growth in new international

marketing projects has to be greater than 100 percent per year." Jens Lundeson, of the

Association in Europe, said "We see growth in this kind of project at 40 percent or better per

year."

Target Market Growth

Click to Enlarge

2.2 SWOT Analysis [back to top]

The SWOT analysis covers strengths, weaknesses, opportunities, and threats. Strengths and

weaknesses are generally internal attributes, which we can address by changing our business.

Opportunities and threats are generally external.

Overall, the mix is exciting. We live in an age of growth, change, and business revolution. The

Internet offers us opportunities and threats. We need to make our dealing with it one of our

biggest strengths, to minimize our weaknesses.

2.2.1 Strengths [back to top]

True expertise. All of our principals know this area very well. Our experience and expertise is

better than anybody we know of in this particular niche area.

Dominance of communications technologies from a users' point of view. We have an excellent

website, secure File Transfer Protocol (FTP) facilities with password protection for sending

and receiving documents from clients, major bandwidth, and an automatic link to training allies

to help clients come up to speed with the facilities we offer. We can even hold Internet

meetings with shared interface and visuals.

Manageable size. We don't have to support a large overhead, and our clients know that we

deliver what we promise ourselves. Our competition, the larger consulting houses, tend to

build on the structure of the major partners doing the selling and younger associates, with far

less experience, actually delivering the consulting.

Contacts. Years of industry experience means a lot of word-of-mouth marketing, contacts, and

networking.

2.2.2 Weaknesses [back to top]

Marketing. As a group, we are good at the direct sales involved in making a close, but we

don't have the resources required to do much general marketing. We will depend on word of

mouth first as our main form of generating leads.

Staff. Without the overhead of staff, we can't leverage on people to develop documents and

presentations, research in detail, and fill in the blanks. We are short on support for telephones,

fax, and email.

Brand. Sometimes a Booz Allen or McKinsey is a safer buy for the executives, in the sense of

"nobody ever got fired for hiring IBM." We are a new entity, we can be perceived as an

innovative -- and therefore risky -- choice.

2.2.3 Opportunities [back to top]

Internet growth. Companies are being dragged into worldwide marketing, like it or not. Growth

rates are very high, opportunities are obvious.

International market growth. Europe and Latin America are booming. Asia has suffered a bit

but is recovering. Manufacturers are anxious to take their new technologies across borders.

Growing red tape involved with hiring full-time employees, especially internationally,

especially at the executive level.

2.2.4 Threats [back to top]

The Internet is a threat as well as an opportunity. Our expertise is about crossing borders,

managing multiple markets, and the problems we solve are being reduced in importance by the

growing availability of information. Specific example: software companies used to charge huge

premiums for software available in the different smaller markets, but their potential customers

are now much more likely to see available prices elsewhere and buy over the net.

The larger, branded competition is recognizing our niche. They are beginning to compete in

our area, recognize our niche. We are no longer alone.

New competitors are developing in new markets. Particularly as the European market grows,

competitors developing in that area become more significant.

2.3 Competition [back to top]

The key element in purchase decisions made at the GDK client level is trust in the

professional reputation and reliability of the consulting firm.

The competition comes in several forms:

1. The most significant competition is no consulting at all, companies choosing to do business

development, channel development and market research in-house. Their own managers do this

on their own, as part of their regular business functions. Our key advantage in competition

with in-house development is that managers are already overloaded with responsibilities; they

don't have time for additional responsibilities in new market development or new channel

development. Also, GDK can approach alliances, vendors, and channels on a confidential

basis, gathering information and making initial contacts in ways that the corporate managers

can't.

2. The high-level prestige management consulting:

XXXXX,XXXXXXXXXXXX,XXXXX-XXXXX, (names omitted to protect confidentiality),

etc. These are essentially generalists who take their name-brand management consulting into

specialty areas. Their other very important weakness is the management structure that has the

partners selling new jobs, and inexperienced associates delivering the work. We compete

against them as experts in our specific fields, and with the guarantee that our clients will have

the top-level people doing the actual work.

3. The third general kind of competitor is the international market research company:

XXXXXXXXX, XXXXXX, XXXX-XXXXX, (names omitted to protect confidentiality), etc.

These companies are formidable competitors for published market research and market forums

but cannot provide the kind of high-level consulting that GDK will provide.

4. The fourth kind of competition is the market-specific smaller house. For example: Nomura

Research in Japan, Select S.A. de C.V. in Mexico (now affiliated with IDC).

5. Sales representation, brokering, and deal catalysts are an ad-hoc business form that will be

defined in detail by the specific nature of each individual case.

2.4 Services [back to top]

Acme offers expertise in channel distribution, channel development, and market development,

sold and packaged in various ways that allow clients to choose their preferred relationship:

these include retainer consulting relationships, project-based consulting, relationship and

alliance brokering, sales representation and market representation, project-based market

research, published market research, and information forum events.

1. Retainer consulting. We represent a client company as an extension of its business

development and market development functions. This begins with complete understanding of

the client company's situation, objectives, and constraints. We then represent the client

company quietly and confidentially, sifting through new market developments and new

opportunities as is appropriate to the client, representing the client in initial talks with possible

allies, vendors, and channels.

2. Project consulting. Proposed and billed on a per-project and per-milestone basis, project

consulting offers a client company a way to harness our specific qualities and use our

expertise to solve specific problems, develop and/or implement plans, and develop specific

information.

3. Market research. Group studies available to selected clients at $5,000 per unit. A group

study is a packaged and published complete study of a specific market, channel, or topic.

Examples might be studies of developing consumer channels in Japan or Mexico, or

implications of changing margins in software.

2.5 Keys to Success [back to top]

Excellence in fulfilling the promise--completely confidential, reliable, trustworthy expertise and

information.

Developing visibility to generate new business leads.

Leveraging from a single pool of expertise into multiple revenue generation opportunities:

retainer consulting, project consulting, market research, and market research published

reports.

2.6 Critical Issues [back to top]

The most critical issue is repeat business. We can't build this company on a faulty foundation;

we have to have a core group of satisfied clients who come back to us on a regular basis. We

can't afford to spend the capital it would take to generate new clients constantly. The repeat

business costs about a tenth as much in sales and marketing as the new client.

Repeat business is built on the correct strategic mix of excellence in delivery, clear

communication of promise and scope, and follow through.

Most of our competitors build on a structure that has the partners selling the jobs and new

hires, bright young people without a lot of experience, delivering. We can't afford to follow

that lead. We can use a staff to leverage some of the footwork and analysis work, but

ultimately our work must be our own.

2.7 Historical Results [back to top]

To analyze our historical data, we've made a projection based on what might have been, had

the partners been involved in a separate company. It is a composite of the combined

consulting of the three main partners.

What we see in the table is that we're taking up a very small portion of the overall consulting

dollar spent in this market. There is a lot of room to grow. We have always been profitable, but

we expect to do much better than we have after we combine our forces.

2.8 Macroenvironment [back to top]

New technology has become the driving force of our market. The Internet is changing

high-tech marketing overnight. While the manufacturers used to deal with distributors in

smaller national markets, nowadays the distributors are terribly concerned about our pricing

and marketing over the Internet.

On one hand, the manufacturers need loyal local allies, good distribution, and value added. On

the other hand, they can't pretend to offer protected markets. The Internet changes the game.

Another major factor is the growth expected in Europe and Latin America. While Asian

markets are hanging back a bit with the lingering effect of recent economic problems, the Latin

American markets are growing smartly as a result of decreasing protectionism, and the

European markets are enjoying the new Eurodollar boom.

3.0 Marketing Strategy [back to top]

Strategy is focus. Our strategy involves focusing on a specific area of expertise in which we

are as strong a group as in any company anywhere in the world. We are true experts in the

introduction of new technology products, especially through channels of distribution.

Acme will focus on three geographical markets; the United States, Europe, and Latin America,

and in limited product segments; personal computers, software, networks,

telecommunications, personal organizers, and technology integration products.

The target customer is usually a manager in a larger corporation, and occasionally an owner or

president of a medium-sized corporation in a high-growth period.

3.1 Mission [back to top]

GDK offers high-tech manufacturers a reliable, high-quality alternative to

in-house resources for business development, market development, and channel development

on an international scale. A true alternative to in-house resources, we offer a very high level of

practical experience, know-how, contacts, and confidentiality. Clients must know that working

with Acme is a more professional, less risky way to develop new areas even than working

completely in-house with their own people. GDK must also be able to maintain financial

balance, charging a high value for its services, and delivering an even higher value to its

clients. We focus on development in the European and Latin American markets, or for

European clients in the United States market.

3.2 Marketing Objectives [back to top]

We need to establish ourselves as experts. This means being quoted in major trade press,

speaking at industry events, and gaining recognition. Our measurable and specific objective is

to be introduced in three major events as established experts in the field of international

market entry.

We need brand-name reference clients. By the end of this year, we need three major brand

names we can cite as clients. We need to be able to reference by name and contact phone

number.

We need at least one client in each of three main regions. United States and Europe for sure,

and also either Latin America or Asia. We can't be who we claim to be without being truly

multi-continental.

3.3 Financial Objectives [back to top]

Sales of $350,000 in 1995 and $1 million by 1997.

Gross margin higher than 80%.

Net income more than 10% of sales by the third year.

3.4 Target Markets [back to top]

As indicated by the previous Table 2.1,Target Market Forecast,we must focus on a few

thousand well-chosen potential customers in the United States, Europe, and Latin America.

These few thousand high-tech manufacturing companies are the key customers for GDK.

3.5 Positioning [back to top]

For high-technology companies who are looking to enter new international markets, GDK

offers a unique team of experienced managers with proven expertise, on a

temporary contract basis. Unlike in-house expertise, GDK is a temporary variable

cost.GDK is specialized on a very focused expertise that is hard to duplicate.

3.6 Strategy Pyramids [back to top]

Our strategy is to focus on our main area of expertise. We have plenty of competition in

international marketing and in product introduction expertise, but nobody can match us when

we stay focused on introducing a high-tech product into channels in international markets.

Our tactics to make this real? First, the quality of work. Second, expertise-based marketing.

Third, we rest on heavy use of the newest technologies in international communications (i.e.

Internet technologies).

The diagram shows how our marketing programs map into the tactics.

3.7 Marketing Mix [back to top]

Ours is a delivery-intensive, word-of-mouth, repeat-business business. We aren't marketing as

much as selling direct. Obviously we know we need to understand our marketing process --

which is why the attention to quotes in magazines, speaking engagements, etc. -- but we are

really selling more than marketing.

In this section, we'll focus on the components of our marketing mix.

3.7.1 Services Offered [back to top]

The service itself is a key component to our marketing mix. Our service should be our best

advertisement. In this case even more so than with many other similar businesses, because

our specialization on channels for international product marketing means we develop contacts

with people who can be our recommenders.

We need to fulfill the promise we make: we take a product across national boundaries into new

markets, explore channels, guide our client through the maze, and establish the relationships

the client needs. This is a very focused deliverable. We aren't just doing international

marketing or marketing consulting; we're getting products into channels.

The service itself is a key to our markets.

3.7.2 Price [back to top]

We need to make sure that our services are adequately priced. Our positioning, as well as our

finances, demands high pricing. When a job is exactly our expertise, we should expect to price

high.

Ultimately, our client will end up spending less on us than on the branded major consultants,

because they will wrap the consulting around a lot of additional research and their standard

packaging that doubles or triples cost. We'll focus in on the exact target and charge more per

day and less for the total job.

We should expect to be much more expensive than the second-tier generalists.

3.7.3 Promotion [back to top]

For promotion, we follow the mainstream thinking about high-end consulting. There are two

main components of promotion:

1. Getting recognized and quoted as experts. Our public relations expense is intended to

position us as the experts the business press calls on for information on international channel

marketing. We need to be quoted in Business Week, Fortune, and the Wall Street Journal, as

well as Wired, Red Herring, Upside, and the like. Along the same lines, we need to get the

speaking engagements at the major trade shows and events.

2. Word of mouth and reference sites. This goes back to our core value, the importance of

fulfilling the promise.

3. The Internet. We need to dominate the Internet, search terms, placement in searchers, etc.

3.7.4 Service [back to top]

Service in this topic refers to our client service -- not what we sell as a service company, but

the service we deliver as an add-on to the basic service we sell. Confusing? Perhaps, but let's

look at client service for a consulting service:

1. First, service begins with how we communicate with the client, during and after the

consulting job. This is where most of our competitors fall down. Far too often the consultants

disappear from the client in what feels like hiding while doing the work. We're going to use the

website in password-protected draft mode so that our clients are always in touch with us.

They can log into the website and see our drafts. We'll give them real service, instead of just

sales.

2. We also need to give much better service to clients after the job: better accessibility to our

work once done. Studies should be available to management; contacts, recommended

channels, information that they own and they can use, when they need it, and when they want

it.

3.8 Marketing Research [back to top]

We need to cover two main elements of market research:

1. Manufacturers. We need to know the market of manufacturers in all three target continents,

including market trends and developments related to manufacturers of personal computers,

peripherals, connectivity and Internet, and software.

2. Channel marketing. We need to know the trends in channel competition, emergence of new

channels, economics, major competitors, new technologies, and major players in all three

continents.

At this stage of our development, our research is mainly secondary research generated by

keeping up with the media, including trade press and the Internet. We should quickly

establish a strong filing system so that we can use the information that appears in secondary

sources and catalog and organize for effective use later on.

4.0 Financials [back to top]

Our plan calls for sales of nearly $600,000 this year growing to $1.8 million by 2009, on

marketing expenses of slightly more than $200,000, which is about 35% of sales. By the last

year in the plan, our marketing expenses of $480,000 will be only 25% of sales.

The plan assumes two important trends:

First, a steady decline in cost of sales and growth in gross margin percentage as we build more

of our resources, as full-time personnel and fixed costs instead of contractors and outside

consultants. That means that as we grow we take on more risk -- if the plan is implemented.

Step by step we'll have to watch the growth of sales relationships that imply the advisability

of taking on more people as partners and employees, instead of as contractors.

Second, a decline in marketing expenses as a percent of sales. The 35% figure we project for

the first year is quite high, unacceptably high except that we are building a reputation and

marketing without the leverage of past marketing, starting from zero. By the fifth year of the

plan, we should be spending 25% of sales on marketing. This is a better figure.

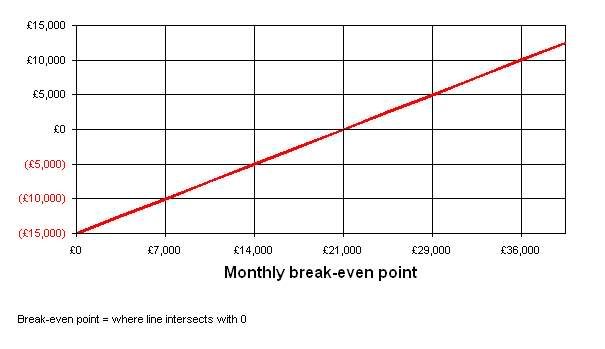

4.1 Break-even Analysis [back to top]

For manufacturers, we have an unusually high variable cost of 30% of sales. This makes sense

for us at this point, because turning to experts on a per-job basis, as long as these are the

people we know and trust, reduces the risk of fixed costs.

This break-even is a reflection of our first year, in which we are building our fulfillment based

on variable cost people instead of fixed-cost people. The risk profile should look very different

by the last year.

Break-even Analysis

Click to Enlarge

Break-even Analysis:

Monthly Units Break-even 21,429

Monthly Revenue Break-even È21,429

Assumptions:

Average Per-Unit Revenue È1.00

Average Per-Unit Variable Cost È0.30

Estimated Monthly Fixed Cost È15,000

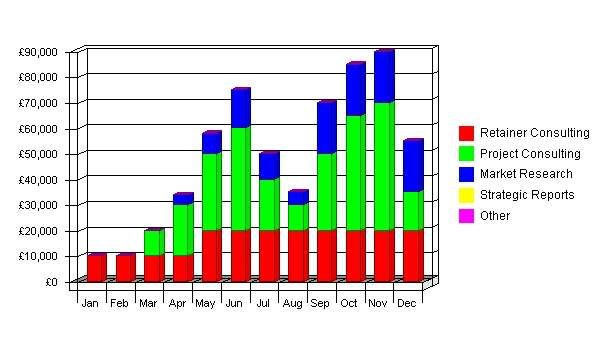

4.2 Sales Forecast [back to top]

Our sales for this start-up period grow from $10,000 per month at the beginning -- retainer

business from our founder, with existing clients -- to $90,000 next fall. The sales

forecast is aggressive, assuming financing for our marketing expense and bringing on partners

and staff as planned.

We intend to continue to increase billings throughout the forecast period, reaching annual

totals increasing from less than $600,000 in the first year to $1.825 million in the fifth.

Monthly Sales Forecast

Click to Enlarge

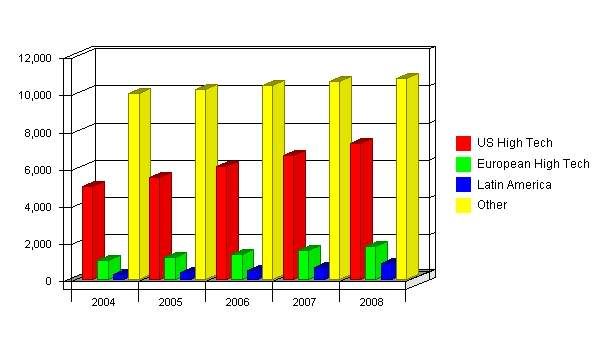

Sales Forecast

Sales 2004 2005 2006

Retainer Consulting È200,000 È350,000 È425,000

Project Consulting È270,000 È325,000 È350,000

Market Research È122,000 È150,000 È200,000

Strategic Reports È0 È50,000 È125,000

Other È0 È25,000 È50,000

Total Sales È592,000 È900,000 È1,150,000

Direct Cost of Sales 2004 2005 2006

Retainer Consulting È30,000 È20,000 È15,000

Project Consulting È45,000 È20,000 È15,000

Market Research È84,000 È86,000 È88,000

Strategic Reports È0 È20,000 È25,000

Other È0 È10,000 È10,000

Subtotal Direct Cost of Sales È159,000 È156,000 È153,000

4.2.1 Sales by Partner [back to top]

As the projection shows, we expect our billing to come from all three of our main partners first.

The partners have relationships that should create these billings at that level.

Later on, we expect the billing to come from additional resources and additional partners, so

the billings attributed to the main three go down as a percentage of the total.

The detail for this table is included in the appendices.

4.2.2 Sales by Segment [back to top]

We expect to focus more on the mainline hardware this first year, but the growth in our

industry is in communications and Internet-related business, so during the five years our

projection shows a continual trend towards the other segment.

The detail for this table is included in the appendices.

4.2.3 Sales by Region [back to top]

In our regional billings, we expect to see the market in Europe growing much more quickly than

in the United States, although the U.S. market starts out much bigger, so that in five years we

are billing in equal portions in the United States and Europe.

The forecast isn't a reflection of total market directly. It also assumes that we are doing what

we have to do to take advantage of the growth potential in Europe. This includes marketing,

developing the practice, and developing the repeat business.

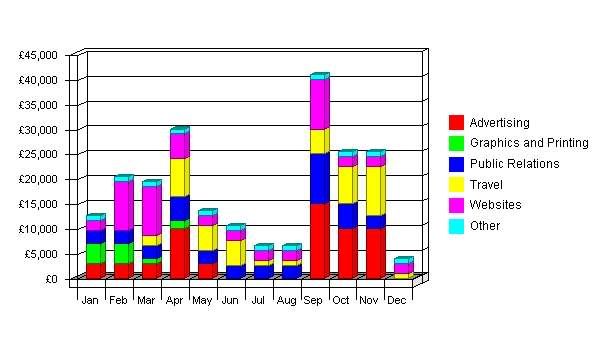

4.3 Expense Forecast [back to top]

Overall we project sales and marketing expenses to more than double from $215,000 this first

year to $480,000 in the fifth year. This compares to sales increasing threefold during the same

period. We believe that effective marketing requires a very high percentage of sales and

marketing expenses to sales during the early years, and that over time we can bring that

percentage down to more acceptable levels.

Expenses divide over four main categories: advertising, public relations, travel, and website. A

smaller budget is included for Graphics and Printing expenses, and we also have a substantial

additional budget for contingencies.

Monthly Expense Budget

Click to Enlarge

Marketing Expense Budget

2004 2005 2006

Advertising È57,000 È65,000 È75,000

Graphics and Printing È10,500 È15,000 È20,000

Public Relations È40,000 È50,000 È55,000

Travel È45,000 È55,000 È60,000

Websites È51,000 È65,000 È75,000

Other È12,000 È25,000 È40,000

------------ ------------ ------------

Total Sales and Marketing Expenses È215,500 È275,000 È325,000

Percent of Sales 36.40% 30.56% 28.26%

4.3.1 Expense by Partner [back to top]

As the table and chart shows -- with more information in the appendices -- most of our

expenses are managed by marketing, not by the partners themselves. Each partner has some

expense allocation to deal with specific client development programs, marketing of expertise,

and related projects.

4.3.2 Expense by Segment [back to top]

As with partners in the preceding topics, most of our expenses go towards general marketing

expenses instead of tailored to a specific segment. This is particularly important for our

development of the industry reputation we need even as the product structures and divisions

change. We expect billings to shift towards communications, but with expenses we need to

market our expertise and let the projects come in their appropriate segments.

4.3.3 Expense by Region [back to top]

Although we don't see our expenses tagged a great deal to specific regions, the projection

does call for an increasing level of expenses directed at the European market. The main bulk of

expenses, however, goes to the "other" category that includes marketing programs directed at

the general marketing of our specific expertise among high-tech companies worldwide.

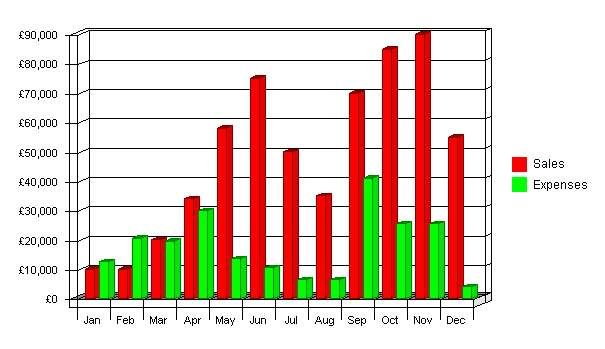

4.4 Linking Expenses to Strategy and Tactics [back to top]

Where we see the strategic match in expenses to sales in the steady increase in relative

spending for Europe and for the communications/Internet segments. These strategic shifts

may be hidden somewhat because of the bulk of spending going into the non-specific areas,

but they are still evident in the sales and expense breakdown by categories.

Our expenses and strategy seem very well matched because we are putting the bulk of

marketing expenses into the key elements for building our leads: quotes in magazines,

magazine articles, speaking engagements, and some very strategic advertising, including

Internet advertising.

Sales vs. Expenses Monthly

Click to Enlarge

4.5 Contribution Margins [back to top]

The contribution margin should increase steadily during the five year plan period, because of

two factors:

1. The cost of sales goes down as we develop the business and grow, bringing on the

expertise we need to fulfill our promise with in-house partners and associates as employees,

rather than contracting expertise. Risk goes up with the increased fixed costs, but the margins

go up too, because cost of sales is less.

2. Our sales and marketing expenses will stabilize. We don't expect to decrease the overall level

of expenses, but they should decline in percentage terms as sales go up.

Given both factors, we project our contribution margin to increase from 36% the first year, to

63% the last year.

5.0 Controls [back to top]

This plan is about implementation, changing the business, and making it better. It is worth

nothing if not implemented. In this chapter we look at specific implementation programs, and

the details that it takes to make it happen.

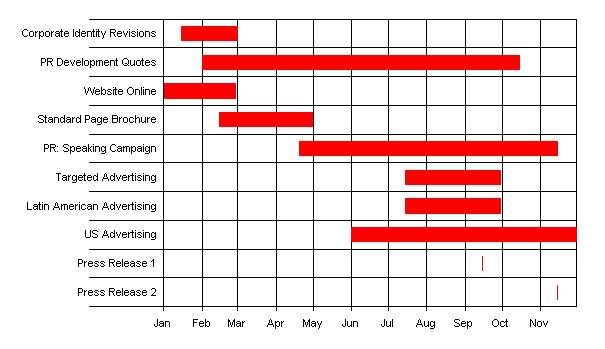

5.1 Implementation [back to top]

The following table and chart identity the key marketing programs, with their managers. Dates

and budgets are clearly established. The managers are informed of their main programs and

they are on board with implementation.

We will be tracking plan-vs.-actual results for each of these programs and discussing them at

our monthly marketing meetings.

The programs will be revised each year. This year's plan includes only the programs to be

implemented this year.

Milestones

Click to Enlarge

Milestones

Milestone Start Date End Date Budget Manager Department

Corporate Identity Revisions 1/15/2000 3/1/2000 È8,000 Tracy All

PR Development Quotes 2/1/2000 10/15/2000 È18,000 Leslie All

Website Online 1/1/2000 2/28/2000 È12,000 Tracy All

Standard Page Brochure 2/15/2000 4/30/2000 È2,500 Tracy All

PR: Speaking Campaign 4/20/2000 11/15/2000 È6,000 Leslie All

Targeted Advertising 7/15/2000 9/30/2000 È2,500 Tracy Europe

Latin American Advertising 7/15/2000 9/30/2000 È1,000 Kelly Latin America

US Advertising 6/1/2000 11/30/2000 È20,000 Tracy US

Press Release 1 9/15/2000 9/15/2000 È5,000 Kelly All

Press Release 2 11/15/2000 11/15/2000 È5,000 Kelly All

Totals È80,000

5.2 Marketing Organization [back to top]

Our marketing department is managed by Gerald Krug, a full-time professional, responsible

to all of the partners as a group but to no specific partner. We need the marketing department

to maintain its professional integrity above and beyond the specific partners, looking out for

our marketing goals and implementing the marketing programs as best fits our strategy.

5.3 Contingency Planning [back to top]

The most likely change in the marketing scheme is a major increase in Internet website traffic

and the importance of website marketing. We will all keep a close eye on website

developments and, if needed, increase our focus on website marketing.

As of this writing, we expect we can develop our niche and focus without direct competition

from the name brand consulting companies. If we attract direct competition operating within

our key area, we should then...(omitted for reasons of confidentiality).

2.1.1 Market Demographics [back to top]

Large manufacturer corporations: Our most important market segment is the large

manufacturer of products, such as Apple, Hewlett-Packard, IBM, Microsoft,

Siemens, or Olivetti. These companies will be calling on GDK for development functions that

are better spun off than managed in-house, for market research, and for market forums.

Medium-sized growth companies: Particularly in software, multimedia, and some related

high-growth fields, GDK will offer an attractive development alternative to the company that

is management constrained and unable to address opportunities in new markets and new

market segments.

Market Analysis

Potential Customers Growth 2004 2005 2006 2007 2008 CAGR

US High Tech 10% 5,000 5,500 6,050 6,655 7,321 10.00%

European High Tech 15% 1,000 1,150 1,323 1,521 1,749 15.00%

Latin America 35% 250 338 456 616 832 35.07%

Other 2% 10,000 10,200 10,404 10,612 10,824 2.00%

Total 6.27% 16,250 17,188 18,233 19,404 20,726 6.27%

2.1.2 Market Needs [back to top]

When a company, like those that are our clients, wants to open a new market, there is a

temporary need for very high-powered expertise. They need to establish distribution, evaluate

distributors' merits and problems, select and open new channels.

Our clients come to us for scalable, temporary expertise. They understand that our kind of

expertise would be very difficult and expensive to get from full-time, permanent employees.

Furthermore, their needs are temporary: the crunch is at the time of opening the new market

and setting up the channel; later on it is not as important.

From the point of view, as managers, our clients come to us at least in part because we reduce

their sense of risk in the management and politics of new market introductions. If things go

wrong, they have experts to blame. If things go right, they get the credit. There's the old

saying that "nobody ever got fired for choosing IBM," meaning choosing a highly respected

visible source for computers. We are that kind of low-risk option for opening new markets.

2.1.3 Market Trends [back to top]

We stand to benefit from some specific market trends:

There is a major trend towards internationalization. The Internet has brought a larger world

into direct communication with the manufacturers. Europe has created a major new unified

market, this time for real. Latin America is healthy and growing. Asia, despite recent setbacks,

is still a very good market. Our potential client base, the manufacturers, wants to expand into

new markets.

Communications technology is a new industry explosion. Also because of the Internet,

growth in communications technology items is explosive. Modems, network cards,

communications software, routers, cables, connectors, all of these are growing at 35% per year

and up. Margins aren't great in the more standard hardware categories, but growth is

enormous.

Contracting, consulting, and ad-hoc management teams are a trend. Even the larger

businesses are turning more frequently to temporary expertise instead of permanent fixed cost

employees. This is the latest new application of the buzzword "scalable." GDK is

an especially attractive alternative to our clients, because of the economic advantages of

variable vs. fixed costs, and the growing liabilities and overhead of taking on long-term

employees.

Market Forecast

Click to Enlarge

2.1.1 Market Demographics [back to top]

Large manufacturer corporations: Our most important market segment is the large

manufacturer of products, such as Apple, Hewlett-Packard, IBM, Microsoft,

Siemens, or Olivetti. These companies will be calling on GDK for development functions that

are better spun off than managed in-house, for market research, and for market forums.

Medium-sized growth companies: Particularly in software, multimedia, and some related

high-growth fields, GDK will offer an attractive development alternative to the company that

is management constrained and unable to address opportunities in new markets and new

market segments.

Market Analysis

Potential Customers Growth 2004 2005 2006 2007 2008 CAGR

US High Tech 10% 5,000 5,500 6,050 6,655 7,321 10.00%

European High Tech 15% 1,000 1,150 1,323 1,521 1,749 15.00%

Latin America 35% 250 338 456 616 832 35.07%

Other 2% 10,000 10,200 10,404 10,612 10,824 2.00%

Total 6.27% 16,250 17,188 18,233 19,404 20,726 6.27%

2.1.2 Market Needs [back to top]

When a company, like those that are our clients, wants to open a new market, there is a

temporary need for very high-powered expertise. They need to establish distribution, evaluate

distributors' merits and problems, select and open new channels.

Our clients come to us for scalable, temporary expertise. They understand that our kind of

expertise would be very difficult and expensive to get from full-time, permanent employees.

Furthermore, their needs are temporary: the crunch is at the time of opening the new market

and setting up the channel; later on it is not as important.

From the point of view, as managers, our clients come to us at least in part because we reduce

their sense of risk in the management and politics of new market introductions. If things go

wrong, they have experts to blame. If things go right, they get the credit. There's the old

saying that "nobody ever got fired for choosing IBM," meaning choosing a highly respected

visible source for computers. We are that kind of low-risk option for opening new markets.

2.1.3 Market Trends [back to top]

We stand to benefit from some specific market trends:

There is a major trend towards internationalization. The Internet has brought a larger world

into direct communication with the manufacturers. Europe has created a major new unified

market, this time for real. Latin America is healthy and growing. Asia, despite recent setbacks,

is still a very good market. Our potential client base, the manufacturers, wants to expand into

new markets.

Communications technology is a new industry explosion. Also because of the Internet,

growth in communications technology items is explosive. Modems, network cards,

communications software, routers, cables, connectors, all of these are growing at 35% per year

and up. Margins aren't great in the more standard hardware categories, but growth is

enormous.

Contracting, consulting, and ad-hoc management teams are a trend. Even the larger

businesses are turning more frequently to temporary expertise instead of permanent fixed cost

employees. This is the latest new application of the buzzword "scalable." GDK is

an especially attractive alternative to our clients, because of the economic advantages of

variable vs. fixed costs, and the growing liabilities and overhead of taking on long-term

employees.

Market Forecast

Click to Enlarge  2.1.4 Market Growth [back to top]

The U.S. Association of Marketing Consultants reports a 30% growth in average revenues for

consultants focusing on marketing of products. We are a subset of this market,

possibly due for even higher growth than the mainstream. The local electronics industry

association in California reports a trend towards additional consulting solutions, as

manufacturers turn to variable cost solutions.

We talked to industry associations in Japan and several in Europe. Overall, the growth in

interest for moving into new markets is phenomenal. Tahahashi Sato, director of the local

association in Tokyo, told us "we don't have statistics, but the growth in new international

marketing projects has to be greater than 100 percent per year." Jens Lundeson, of the

Association in Europe, said "We see growth in this kind of project at 40 percent or better per

year."

Target Market Growth

Click to Enlarge

2.1.4 Market Growth [back to top]

The U.S. Association of Marketing Consultants reports a 30% growth in average revenues for

consultants focusing on marketing of products. We are a subset of this market,

possibly due for even higher growth than the mainstream. The local electronics industry

association in California reports a trend towards additional consulting solutions, as

manufacturers turn to variable cost solutions.

We talked to industry associations in Japan and several in Europe. Overall, the growth in

interest for moving into new markets is phenomenal. Tahahashi Sato, director of the local

association in Tokyo, told us "we don't have statistics, but the growth in new international

marketing projects has to be greater than 100 percent per year." Jens Lundeson, of the

Association in Europe, said "We see growth in this kind of project at 40 percent or better per

year."

Target Market Growth

Click to Enlarge  2.2 SWOT Analysis [back to top]

The SWOT analysis covers strengths, weaknesses, opportunities, and threats. Strengths and

weaknesses are generally internal attributes, which we can address by changing our business.

Opportunities and threats are generally external.

Overall, the mix is exciting. We live in an age of growth, change, and business revolution. The

Internet offers us opportunities and threats. We need to make our dealing with it one of our

biggest strengths, to minimize our weaknesses.

2.2.1 Strengths [back to top]

True expertise. All of our principals know this area very well. Our experience and expertise is

better than anybody we know of in this particular niche area.

Dominance of communications technologies from a users' point of view. We have an excellent

website, secure File Transfer Protocol (FTP) facilities with password protection for sending

and receiving documents from clients, major bandwidth, and an automatic link to training allies

to help clients come up to speed with the facilities we offer. We can even hold Internet

meetings with shared interface and visuals.

Manageable size. We don't have to support a large overhead, and our clients know that we

deliver what we promise ourselves. Our competition, the larger consulting houses, tend to

build on the structure of the major partners doing the selling and younger associates, with far

less experience, actually delivering the consulting.

Contacts. Years of industry experience means a lot of word-of-mouth marketing, contacts, and

networking.

2.2.2 Weaknesses [back to top]

Marketing. As a group, we are good at the direct sales involved in making a close, but we

don't have the resources required to do much general marketing. We will depend on word of

mouth first as our main form of generating leads.

Staff. Without the overhead of staff, we can't leverage on people to develop documents and

presentations, research in detail, and fill in the blanks. We are short on support for telephones,

fax, and email.

Brand. Sometimes a Booz Allen or McKinsey is a safer buy for the executives, in the sense of

"nobody ever got fired for hiring IBM." We are a new entity, we can be perceived as an

innovative -- and therefore risky -- choice.

2.2.3 Opportunities [back to top]

Internet growth. Companies are being dragged into worldwide marketing, like it or not. Growth

rates are very high, opportunities are obvious.

International market growth. Europe and Latin America are booming. Asia has suffered a bit

but is recovering. Manufacturers are anxious to take their new technologies across borders.

Growing red tape involved with hiring full-time employees, especially internationally,

especially at the executive level.

2.2.4 Threats [back to top]

The Internet is a threat as well as an opportunity. Our expertise is about crossing borders,

managing multiple markets, and the problems we solve are being reduced in importance by the

growing availability of information. Specific example: software companies used to charge huge

premiums for software available in the different smaller markets, but their potential customers

are now much more likely to see available prices elsewhere and buy over the net.

The larger, branded competition is recognizing our niche. They are beginning to compete in

our area, recognize our niche. We are no longer alone.

New competitors are developing in new markets. Particularly as the European market grows,

competitors developing in that area become more significant.

2.3 Competition [back to top]

The key element in purchase decisions made at the GDK client level is trust in the

professional reputation and reliability of the consulting firm.

The competition comes in several forms:

1. The most significant competition is no consulting at all, companies choosing to do business

development, channel development and market research in-house. Their own managers do this

on their own, as part of their regular business functions. Our key advantage in competition

with in-house development is that managers are already overloaded with responsibilities; they

don't have time for additional responsibilities in new market development or new channel

development. Also, GDK can approach alliances, vendors, and channels on a confidential

basis, gathering information and making initial contacts in ways that the corporate managers

can't.

2. The high-level prestige management consulting:

XXXXX,XXXXXXXXXXXX,XXXXX-XXXXX, (names omitted to protect confidentiality),

etc. These are essentially generalists who take their name-brand management consulting into

specialty areas. Their other very important weakness is the management structure that has the

partners selling new jobs, and inexperienced associates delivering the work. We compete

against them as experts in our specific fields, and with the guarantee that our clients will have

the top-level people doing the actual work.

3. The third general kind of competitor is the international market research company:

XXXXXXXXX, XXXXXX, XXXX-XXXXX, (names omitted to protect confidentiality), etc.

These companies are formidable competitors for published market research and market forums

but cannot provide the kind of high-level consulting that GDK will provide.

4. The fourth kind of competition is the market-specific smaller house. For example: Nomura

Research in Japan, Select S.A. de C.V. in Mexico (now affiliated with IDC).

5. Sales representation, brokering, and deal catalysts are an ad-hoc business form that will be

defined in detail by the specific nature of each individual case.

2.4 Services [back to top]

Acme offers expertise in channel distribution, channel development, and market development,

sold and packaged in various ways that allow clients to choose their preferred relationship:

these include retainer consulting relationships, project-based consulting, relationship and

alliance brokering, sales representation and market representation, project-based market

research, published market research, and information forum events.

1. Retainer consulting. We represent a client company as an extension of its business

development and market development functions. This begins with complete understanding of

the client company's situation, objectives, and constraints. We then represent the client

company quietly and confidentially, sifting through new market developments and new

opportunities as is appropriate to the client, representing the client in initial talks with possible

allies, vendors, and channels.

2. Project consulting. Proposed and billed on a per-project and per-milestone basis, project

consulting offers a client company a way to harness our specific qualities and use our

expertise to solve specific problems, develop and/or implement plans, and develop specific

information.

3. Market research. Group studies available to selected clients at $5,000 per unit. A group

study is a packaged and published complete study of a specific market, channel, or topic.

Examples might be studies of developing consumer channels in Japan or Mexico, or

implications of changing margins in software.

2.5 Keys to Success [back to top]

Excellence in fulfilling the promise--completely confidential, reliable, trustworthy expertise and

information.

Developing visibility to generate new business leads.

Leveraging from a single pool of expertise into multiple revenue generation opportunities:

retainer consulting, project consulting, market research, and market research published

reports.

2.6 Critical Issues [back to top]

The most critical issue is repeat business. We can't build this company on a faulty foundation;

we have to have a core group of satisfied clients who come back to us on a regular basis. We

can't afford to spend the capital it would take to generate new clients constantly. The repeat

business costs about a tenth as much in sales and marketing as the new client.

Repeat business is built on the correct strategic mix of excellence in delivery, clear

communication of promise and scope, and follow through.

Most of our competitors build on a structure that has the partners selling the jobs and new

hires, bright young people without a lot of experience, delivering. We can't afford to follow

that lead. We can use a staff to leverage some of the footwork and analysis work, but

ultimately our work must be our own.

2.7 Historical Results [back to top]

To analyze our historical data, we've made a projection based on what might have been, had

the partners been involved in a separate company. It is a composite of the combined

consulting of the three main partners.

What we see in the table is that we're taking up a very small portion of the overall consulting

dollar spent in this market. There is a lot of room to grow. We have always been profitable, but

we expect to do much better than we have after we combine our forces.

2.8 Macroenvironment [back to top]

New technology has become the driving force of our market. The Internet is changing

high-tech marketing overnight. While the manufacturers used to deal with distributors in

smaller national markets, nowadays the distributors are terribly concerned about our pricing

and marketing over the Internet.

On one hand, the manufacturers need loyal local allies, good distribution, and value added. On

the other hand, they can't pretend to offer protected markets. The Internet changes the game.

Another major factor is the growth expected in Europe and Latin America. While Asian

markets are hanging back a bit with the lingering effect of recent economic problems, the Latin

American markets are growing smartly as a result of decreasing protectionism, and the

European markets are enjoying the new Eurodollar boom.

3.0 Marketing Strategy [back to top]

Strategy is focus. Our strategy involves focusing on a specific area of expertise in which we

are as strong a group as in any company anywhere in the world. We are true experts in the

introduction of new technology products, especially through channels of distribution.

Acme will focus on three geographical markets; the United States, Europe, and Latin America,

and in limited product segments; personal computers, software, networks,

telecommunications, personal organizers, and technology integration products.

The target customer is usually a manager in a larger corporation, and occasionally an owner or

president of a medium-sized corporation in a high-growth period.

3.1 Mission [back to top]

GDK offers high-tech manufacturers a reliable, high-quality alternative to

in-house resources for business development, market development, and channel development

on an international scale. A true alternative to in-house resources, we offer a very high level of

practical experience, know-how, contacts, and confidentiality. Clients must know that working

with Acme is a more professional, less risky way to develop new areas even than working

completely in-house with their own people. GDK must also be able to maintain financial

balance, charging a high value for its services, and delivering an even higher value to its

clients. We focus on development in the European and Latin American markets, or for

European clients in the United States market.

3.2 Marketing Objectives [back to top]

We need to establish ourselves as experts. This means being quoted in major trade press,

speaking at industry events, and gaining recognition. Our measurable and specific objective is

to be introduced in three major events as established experts in the field of international

market entry.

We need brand-name reference clients. By the end of this year, we need three major brand

names we can cite as clients. We need to be able to reference by name and contact phone

number.

We need at least one client in each of three main regions. United States and Europe for sure,

and also either Latin America or Asia. We can't be who we claim to be without being truly

multi-continental.

3.3 Financial Objectives [back to top]

Sales of $350,000 in 1995 and $1 million by 1997.

Gross margin higher than 80%.

Net income more than 10% of sales by the third year.

3.4 Target Markets [back to top]

As indicated by the previous Table 2.1,Target Market Forecast,we must focus on a few

thousand well-chosen potential customers in the United States, Europe, and Latin America.

These few thousand high-tech manufacturing companies are the key customers for GDK.

3.5 Positioning [back to top]

For high-technology companies who are looking to enter new international markets, GDK

offers a unique team of experienced managers with proven expertise, on a

temporary contract basis. Unlike in-house expertise, GDK is a temporary variable

cost.GDK is specialized on a very focused expertise that is hard to duplicate.

3.6 Strategy Pyramids [back to top]

Our strategy is to focus on our main area of expertise. We have plenty of competition in

international marketing and in product introduction expertise, but nobody can match us when

we stay focused on introducing a high-tech product into channels in international markets.

Our tactics to make this real? First, the quality of work. Second, expertise-based marketing.

Third, we rest on heavy use of the newest technologies in international communications (i.e.

Internet technologies).

The diagram shows how our marketing programs map into the tactics.

3.7 Marketing Mix [back to top]

Ours is a delivery-intensive, word-of-mouth, repeat-business business. We aren't marketing as

much as selling direct. Obviously we know we need to understand our marketing process --

which is why the attention to quotes in magazines, speaking engagements, etc. -- but we are

really selling more than marketing.

In this section, we'll focus on the components of our marketing mix.

3.7.1 Services Offered [back to top]

The service itself is a key component to our marketing mix. Our service should be our best

advertisement. In this case even more so than with many other similar businesses, because

our specialization on channels for international product marketing means we develop contacts

with people who can be our recommenders.

We need to fulfill the promise we make: we take a product across national boundaries into new

markets, explore channels, guide our client through the maze, and establish the relationships

the client needs. This is a very focused deliverable. We aren't just doing international

marketing or marketing consulting; we're getting products into channels.

The service itself is a key to our markets.

3.7.2 Price [back to top]

We need to make sure that our services are adequately priced. Our positioning, as well as our

finances, demands high pricing. When a job is exactly our expertise, we should expect to price

high.

Ultimately, our client will end up spending less on us than on the branded major consultants,

because they will wrap the consulting around a lot of additional research and their standard

packaging that doubles or triples cost. We'll focus in on the exact target and charge more per

day and less for the total job.

We should expect to be much more expensive than the second-tier generalists.

3.7.3 Promotion [back to top]

For promotion, we follow the mainstream thinking about high-end consulting. There are two

main components of promotion:

1. Getting recognized and quoted as experts. Our public relations expense is intended to

position us as the experts the business press calls on for information on international channel

marketing. We need to be quoted in Business Week, Fortune, and the Wall Street Journal, as

well as Wired, Red Herring, Upside, and the like. Along the same lines, we need to get the

speaking engagements at the major trade shows and events.

2. Word of mouth and reference sites. This goes back to our core value, the importance of

fulfilling the promise.

3. The Internet. We need to dominate the Internet, search terms, placement in searchers, etc.

3.7.4 Service [back to top]

Service in this topic refers to our client service -- not what we sell as a service company, but

the service we deliver as an add-on to the basic service we sell. Confusing? Perhaps, but let's

look at client service for a consulting service:

1. First, service begins with how we communicate with the client, during and after the

consulting job. This is where most of our competitors fall down. Far too often the consultants

disappear from the client in what feels like hiding while doing the work. We're going to use the

website in password-protected draft mode so that our clients are always in touch with us.

They can log into the website and see our drafts. We'll give them real service, instead of just

sales.

2. We also need to give much better service to clients after the job: better accessibility to our

work once done. Studies should be available to management; contacts, recommended

channels, information that they own and they can use, when they need it, and when they want

it.

3.8 Marketing Research [back to top]

We need to cover two main elements of market research:

1. Manufacturers. We need to know the market of manufacturers in all three target continents,

including market trends and developments related to manufacturers of personal computers,

peripherals, connectivity and Internet, and software.

2. Channel marketing. We need to know the trends in channel competition, emergence of new

channels, economics, major competitors, new technologies, and major players in all three

continents.

At this stage of our development, our research is mainly secondary research generated by

keeping up with the media, including trade press and the Internet. We should quickly

establish a strong filing system so that we can use the information that appears in secondary

sources and catalog and organize for effective use later on.

4.0 Financials [back to top]

Our plan calls for sales of nearly $600,000 this year growing to $1.8 million by 2009, on

marketing expenses of slightly more than $200,000, which is about 35% of sales. By the last

year in the plan, our marketing expenses of $480,000 will be only 25% of sales.

The plan assumes two important trends:

First, a steady decline in cost of sales and growth in gross margin percentage as we build more

of our resources, as full-time personnel and fixed costs instead of contractors and outside

consultants. That means that as we grow we take on more risk -- if the plan is implemented.

Step by step we'll have to watch the growth of sales relationships that imply the advisability

of taking on more people as partners and employees, instead of as contractors.

Second, a decline in marketing expenses as a percent of sales. The 35% figure we project for

the first year is quite high, unacceptably high except that we are building a reputation and

marketing without the leverage of past marketing, starting from zero. By the fifth year of the

plan, we should be spending 25% of sales on marketing. This is a better figure.

4.1 Break-even Analysis [back to top]

For manufacturers, we have an unusually high variable cost of 30% of sales. This makes sense

for us at this point, because turning to experts on a per-job basis, as long as these are the

people we know and trust, reduces the risk of fixed costs.

This break-even is a reflection of our first year, in which we are building our fulfillment based

on variable cost people instead of fixed-cost people. The risk profile should look very different

by the last year.

Break-even Analysis

Click to Enlarge

2.2 SWOT Analysis [back to top]

The SWOT analysis covers strengths, weaknesses, opportunities, and threats. Strengths and

weaknesses are generally internal attributes, which we can address by changing our business.

Opportunities and threats are generally external.

Overall, the mix is exciting. We live in an age of growth, change, and business revolution. The

Internet offers us opportunities and threats. We need to make our dealing with it one of our

biggest strengths, to minimize our weaknesses.

2.2.1 Strengths [back to top]

True expertise. All of our principals know this area very well. Our experience and expertise is

better than anybody we know of in this particular niche area.

Dominance of communications technologies from a users' point of view. We have an excellent

website, secure File Transfer Protocol (FTP) facilities with password protection for sending

and receiving documents from clients, major bandwidth, and an automatic link to training allies

to help clients come up to speed with the facilities we offer. We can even hold Internet

meetings with shared interface and visuals.

Manageable size. We don't have to support a large overhead, and our clients know that we

deliver what we promise ourselves. Our competition, the larger consulting houses, tend to

build on the structure of the major partners doing the selling and younger associates, with far

less experience, actually delivering the consulting.

Contacts. Years of industry experience means a lot of word-of-mouth marketing, contacts, and

networking.

2.2.2 Weaknesses [back to top]

Marketing. As a group, we are good at the direct sales involved in making a close, but we

don't have the resources required to do much general marketing. We will depend on word of

mouth first as our main form of generating leads.

Staff. Without the overhead of staff, we can't leverage on people to develop documents and

presentations, research in detail, and fill in the blanks. We are short on support for telephones,

fax, and email.

Brand. Sometimes a Booz Allen or McKinsey is a safer buy for the executives, in the sense of

"nobody ever got fired for hiring IBM." We are a new entity, we can be perceived as an

innovative -- and therefore risky -- choice.

2.2.3 Opportunities [back to top]

Internet growth. Companies are being dragged into worldwide marketing, like it or not. Growth

rates are very high, opportunities are obvious.

International market growth. Europe and Latin America are booming. Asia has suffered a bit

but is recovering. Manufacturers are anxious to take their new technologies across borders.

Growing red tape involved with hiring full-time employees, especially internationally,

especially at the executive level.

2.2.4 Threats [back to top]

The Internet is a threat as well as an opportunity. Our expertise is about crossing borders,

managing multiple markets, and the problems we solve are being reduced in importance by the

growing availability of information. Specific example: software companies used to charge huge

premiums for software available in the different smaller markets, but their potential customers

are now much more likely to see available prices elsewhere and buy over the net.

The larger, branded competition is recognizing our niche. They are beginning to compete in

our area, recognize our niche. We are no longer alone.

New competitors are developing in new markets. Particularly as the European market grows,

competitors developing in that area become more significant.

2.3 Competition [back to top]

The key element in purchase decisions made at the GDK client level is trust in the

professional reputation and reliability of the consulting firm.

The competition comes in several forms:

1. The most significant competition is no consulting at all, companies choosing to do business

development, channel development and market research in-house. Their own managers do this

on their own, as part of their regular business functions. Our key advantage in competition

with in-house development is that managers are already overloaded with responsibilities; they

don't have time for additional responsibilities in new market development or new channel

development. Also, GDK can approach alliances, vendors, and channels on a confidential

basis, gathering information and making initial contacts in ways that the corporate managers

can't.

2. The high-level prestige management consulting:

XXXXX,XXXXXXXXXXXX,XXXXX-XXXXX, (names omitted to protect confidentiality),

etc. These are essentially generalists who take their name-brand management consulting into

specialty areas. Their other very important weakness is the management structure that has the

partners selling new jobs, and inexperienced associates delivering the work. We compete

against them as experts in our specific fields, and with the guarantee that our clients will have

the top-level people doing the actual work.

3. The third general kind of competitor is the international market research company:

XXXXXXXXX, XXXXXX, XXXX-XXXXX, (names omitted to protect confidentiality), etc.

These companies are formidable competitors for published market research and market forums

but cannot provide the kind of high-level consulting that GDK will provide.

4. The fourth kind of competition is the market-specific smaller house. For example: Nomura

Research in Japan, Select S.A. de C.V. in Mexico (now affiliated with IDC).

5. Sales representation, brokering, and deal catalysts are an ad-hoc business form that will be

defined in detail by the specific nature of each individual case.

2.4 Services [back to top]

Acme offers expertise in channel distribution, channel development, and market development,

sold and packaged in various ways that allow clients to choose their preferred relationship:

these include retainer consulting relationships, project-based consulting, relationship and

alliance brokering, sales representation and market representation, project-based market

research, published market research, and information forum events.

1. Retainer consulting. We represent a client company as an extension of its business

development and market development functions. This begins with complete understanding of

the client company's situation, objectives, and constraints. We then represent the client

company quietly and confidentially, sifting through new market developments and new

opportunities as is appropriate to the client, representing the client in initial talks with possible

allies, vendors, and channels.

2. Project consulting. Proposed and billed on a per-project and per-milestone basis, project

consulting offers a client company a way to harness our specific qualities and use our

expertise to solve specific problems, develop and/or implement plans, and develop specific

information.

3. Market research. Group studies available to selected clients at $5,000 per unit. A group

study is a packaged and published complete study of a specific market, channel, or topic.

Examples might be studies of developing consumer channels in Japan or Mexico, or

implications of changing margins in software.

2.5 Keys to Success [back to top]

Excellence in fulfilling the promise--completely confidential, reliable, trustworthy expertise and

information.

Developing visibility to generate new business leads.

Leveraging from a single pool of expertise into multiple revenue generation opportunities:

retainer consulting, project consulting, market research, and market research published

reports.

2.6 Critical Issues [back to top]

The most critical issue is repeat business. We can't build this company on a faulty foundation;

we have to have a core group of satisfied clients who come back to us on a regular basis. We

can't afford to spend the capital it would take to generate new clients constantly. The repeat

business costs about a tenth as much in sales and marketing as the new client.

Repeat business is built on the correct strategic mix of excellence in delivery, clear

communication of promise and scope, and follow through.

Most of our competitors build on a structure that has the partners selling the jobs and new

hires, bright young people without a lot of experience, delivering. We can't afford to follow

that lead. We can use a staff to leverage some of the footwork and analysis work, but

ultimately our work must be our own.

2.7 Historical Results [back to top]

To analyze our historical data, we've made a projection based on what might have been, had

the partners been involved in a separate company. It is a composite of the combined

consulting of the three main partners.

What we see in the table is that we're taking up a very small portion of the overall consulting

dollar spent in this market. There is a lot of room to grow. We have always been profitable, but

we expect to do much better than we have after we combine our forces.

2.8 Macroenvironment [back to top]

New technology has become the driving force of our market. The Internet is changing

high-tech marketing overnight. While the manufacturers used to deal with distributors in

smaller national markets, nowadays the distributors are terribly concerned about our pricing

and marketing over the Internet.

On one hand, the manufacturers need loyal local allies, good distribution, and value added. On

the other hand, they can't pretend to offer protected markets. The Internet changes the game.

Another major factor is the growth expected in Europe and Latin America. While Asian

markets are hanging back a bit with the lingering effect of recent economic problems, the Latin

American markets are growing smartly as a result of decreasing protectionism, and the

European markets are enjoying the new Eurodollar boom.

3.0 Marketing Strategy [back to top]

Strategy is focus. Our strategy involves focusing on a specific area of expertise in which we

are as strong a group as in any company anywhere in the world. We are true experts in the